Financial institutions stand as frontline defenders against money laundering, a pervasive threat to both their integrity and the broader financial system. To fortify defenses, laws like the Bank Secrecy Act (BSA) and the USA PATRIOT Act have mandated anti-money laundering (AML) measures, including robust Customer Identification Programs (CIP). In this article, we unravel the essence of CIP rules, their origins, requirements, and implications for financial entities.

Understanding the Genesis of CIP Rules

The genesis of CIP rules can be traced back to Section 326 of the USA PATRIOT Act, post the 9/11 terrorist attacks. This directive mandated U.S. financial institutions to establish a CIP, formalized by the Financial Crimes Enforcement Network (FinCEN) in 2003. Embedded within an institution’s broader AML compliance framework, a CIP serves as a pivotal tool to verify the identities of customers and comprehend the intricacies of their financial dealings.

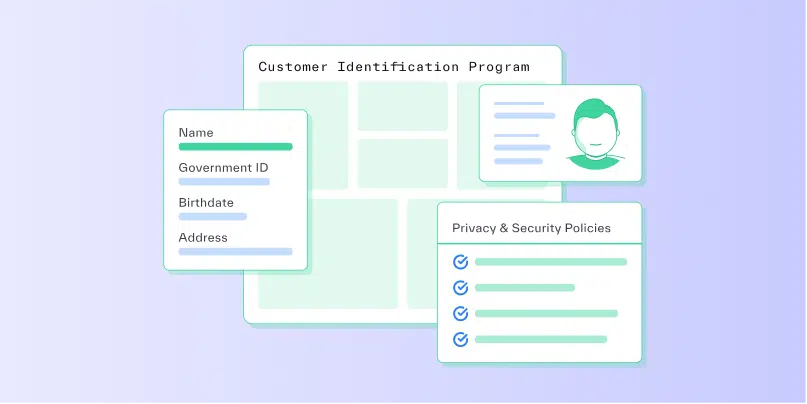

Deciphering the Core Components of a Customer Identification Program

A CIP is not merely a procedural formality but a structured approach to verifying customer identities and anticipating transaction patterns. It entails:

1. Documentation of Account Opening Procedures: Clearly outline the information to be collected from each customer.

2. Implementation of Risk-Based Identity Verification Procedures: Tailored to the institution’s risk profile and practicality, encompassing documentary, non-documentary, or hybrid verification methods.

3. Recordkeeping Obligations: Capturing and retaining customer identity information for a stipulated period, fostering transparency and auditability.

4. Scrutiny against Government Lists: Cross-referencing customer identities with official government lists to mitigate risks.

5. Provision of Notice to Customers: Ensuring transparency by notifying customers of identity verification processes.

Scope and Applicability of CIP Requirements

The mandate of CIP rules extends to a broad spectrum of financial institutions, including banks, credit unions, insurance companies, broker-dealers, and more. While regulatory requirements prescribe a minimum threshold, institutions are afforded the flexibility to tailor their CIP to align with their size, geographic footprint, business complexity, and risk appetite. This ensures a pragmatic and risk-sensitive approach to customer identification.

Key Considerations and Record Retention

Under the CIP rule, institutions must diligently verify the identities of new customers, while maintaining a reasonable belief of existing customer identities. The definition of a “customer” is delineated within the rule, emphasizing ongoing banking relationships over one-time transactions. Institutions may also rely on third-party entities for identity verification, provided compliance obligations are met. Record retention obligations mandate the preservation of customer identity information for a stipulated duration, ensuring historical visibility and auditability.

Embracing Automation for Enhanced Compliance

Given the evolving landscape of financial crime, manual processes offer limited efficacy in combating sophisticated money laundering schemes. Ahrvo Comply offers a suite of automated compliance solutions tailored to address CIP requirements, from identity verification to real-time transaction monitoring. By harnessing automation, financial institutions can fortify their AML defenses, detect high-risk relationships, and foster a culture of compliance.

Conclusion

As money laundering schemes evolve in complexity, financial institutions must fortify their defenses with robust AML measures. Ahrvo Comply stands as a trusted ally, offering cutting-edge solutions to navigate CIP requirements and mitigate money laundering risks. To embark on a journey towards enhanced compliance and risk management, connect with an Ahrvo Comply representative today. Contact Us to learn more about Ahrvo Comply.