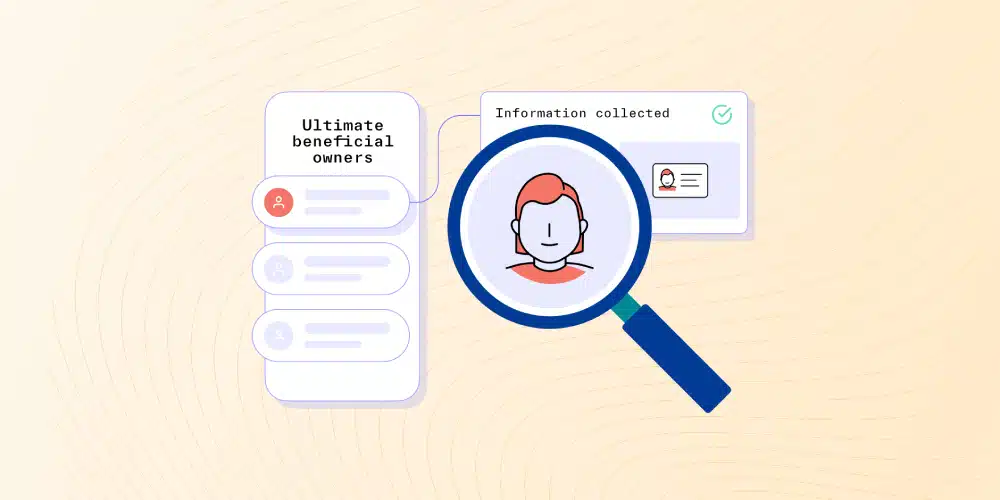

Ultimate Beneficial Ownership (UBO) serves as a cornerstone in the fight against financial crimes, particularly money laundering and terrorist financing. It refers to the identification of the natural person who ultimately owns or controls a legal entity, such as a company or trust. This concept is pivotal for financial services businesses striving to comply with anti-money laundering (AML) regulations, as it unveils the true owners of entities utilizing their platforms and services. By discerning the UBO, businesses gain crucial insights into the risk of fraud, corruption, and illicit activity associated with specific customers or transactions.

Importance of UBO Identification for AML Compliance:

The significance of UBO identification lies in its ability to unravel complex ownership structures and trace the flow of funds back to their source. Through this process, businesses can identify potential conflicts of interest, instances of corruption, or other risks that may pose threats to their operations. Compliance with AML regulations mandates robust procedures to identify and verify the beneficial owners of customers. This includes collecting comprehensive information on ownership and control structures, verifying UBO identity using reliable sources, conducting ongoing monitoring, and promptly reporting any suspicious activities or transactions.

UBO Identification Requirements Under U.S. Regulations:

In the United States, UBO identification is not just a best practice but a legal requirement enforced by the Bank Secrecy Act (BSA) and related regulations issued by the Financial Crimes Enforcement Network (FinCEN). Specifically, the Customer Due Diligence Final Rule, also known as the CDD Rule, mandates financial institutions to establish and implement procedures to identify and verify the beneficial owners of their customers. These procedures entail collecting detailed information on customers’ ownership and control structure, including the names, addresses, and identification numbers of UBOs.

Financial institutions are also obligated to verify the identity of UBOs using reliable and independent sources, such as government-issued identification documents or public registers. Additionally, they must conduct ongoing monitoring of customers and their UBOs to identify any changes in their circumstances or behavior that may indicate potential risks or illicit activities, and report any suspicious activities or transactions to the appropriate authorities as required by law.

Challenges in UBO Screening:

Despite its critical importance, financial services businesses encounter several challenges in implementing compliant and cost-effective UBO identification processes. These challenges include the presence of complex ownership structures, the absence of standardized and reliable data sources, and the dynamic nature of UBO information. Complex ownership structures, including shell companies, nominee shareholders, and bearer shares, often obscure the true ownership of legal entities, making it difficult to trace the ultimate beneficial owner.

Moreover, the absence of a single, comprehensive source of UBO information in the United States requires companies to rely on multiple, sometimes inconsistent, sources to verify UBO information. Furthermore, the dynamic nature of UBO information, with legal entities’ ownership and control structure subject to frequent changes due to mergers, acquisitions, or other events, necessitates continuous monitoring and updating of UBO information to ensure accuracy and relevance.

Overcoming UBO Compliance Challenges:

To overcome these challenges, financial institutions should adopt a risk-based approach to their AML processes, tailoring them to the level of risk each customer or transaction represents. This entails implementing customer and activity risk scoring mechanisms to analyze the risk posed by each customer based on their activity patterns and other factors, and tailoring Know Your Customer identification and verification procedures accordingly. Additionally, financial institutions should consider implementing enhanced due diligence measures for high-risk customers to verify their identity and assess their risk.

This may include obtaining more detailed information on the ownership and control structure, conducting background checks, or consulting external databases and watchlists. Moreover, companies should establish robust procedures for regular monitoring and updating of customer and UBO information to identify any changes in their circumstances or behavior that may indicate potential risks or illicit activities. By adopting these strategies, financial institutions can enhance the efficiency and effectiveness of their UBO identification processes, ensuring compliance with AML regulations while mitigating risks associated with financial crimes.

Conclusion:

In conclusion, identifying the ultimate beneficial owner of customers is not merely a compliance requirement but a critical component of financial institutions’ efforts to combat financial crimes. While the process may impose substantial workloads, costs, and complexity on businesses, it is indispensable for avoiding the risk of non-compliance with AML regulations. Alessa, with its comprehensive AML compliance software solution, offers a range of tools that streamline compliance processes, reduce costs, and enhance effectiveness.

From risk scoring and identity verification to state-of-the-art transaction monitoring, Ahrvo Comply empowers financial institutions to identify and mitigate risks associated with financial crimes, thereby safeguarding their operations and reputation. Contact Us to learn more about Ahrvo Comply.